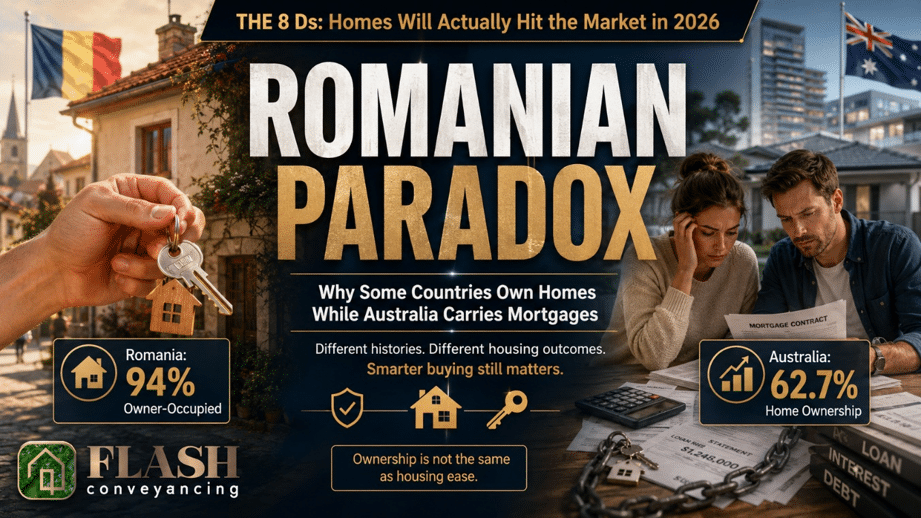

Australia talks a lot about home ownership as a national goal, but the numbers show that our version of ownership is still heavily tied to debt. Ray White’s economic review for April 2026 used OECD housing tenure data to place Australia’s total home ownership rate at 62.7 per cent, below the OECD average of 70.1 per cent. That figure shows home ownership remains part of the Australian story, but it also masks a tougher reality: many Australian owners are still paying off large mortgages rather than owning their homes outright.

Compare that with Romania. Eurostat’s 2025 housing publication found Romania had the highest home ownership rate in the European Union, with 94% of people living in owner-occupied housing in 2024, ahead of Slovakia at 93%, Hungary at 92% and Croatia at 91%. The OECD’s housing tenure data also points to unusually high levels of outright ownership in Central and Eastern Europe, largely because many tenants were able to buy state-owned dwellings at very low prices after the fall of communist regimes. In the OECD dataset, around 94% of Romanian households owned their homes outright.

That can be a confronting comparison for Australian buyers. In Australia, the traditional pathway is to save a deposit, secure finance, repay a mortgage over decades and eventually reach outright ownership later in life. In Romania and parts of Eastern Europe, the ownership profile was shaped by a completely different historical event: the transfer of state-owned housing into private hands during the early 1990s. It was not simply a matter of better budgeting, cheaper homes or higher wages. It came from a very different political and economic system.

That said, the Romanian model should not be romanticised. Ownership does not automatically mean better housing quality or stronger financial security. Eurostat also reported that Romania had one of the highest overcrowding rates in the EU in 2024, at 41%, along with one of the lowest rates of under-occupied housing, at 7%. In other words, many households may own their homes outright, but that does not necessarily mean their housing conditions are superior to those in Australia.

For buyers in NSW, the practical lesson is not to wish for another country’s history, but to make smarter decisions within the system we actually have. Buying property is not simply a lifestyle choice; it is a legal and financial commitment secured against title. NSW Government guidance explains that conveyancing involves the legal work required to prepare contracts, mortgages and related documents, and most people use a licensed conveyancer or solicitor to manage the process. Settlement is generally when the balance of the purchase price is paid and legal ownership transfers to the buyer.

That is where proper legal guidance matters. Flash Conveyancing understands that Australian buyers are navigating a very different housing environment from previous generations. Julian and Renee cannot remove interest rates, lender requirements or deposit hurdles, but they can help buyers understand exactly what they are signing, what risks appear in the contract, what affects the title and what needs to be resolved before settlement takes place.

Flash Conveyancing Advice

The Australian Dream today is less about owning a home quickly and more about owning it wisely. In a market built around long-term mortgages and rising financial pressure, strong legal foundations matter from day one. Before you exchange contracts, make sure you understand the title, the risks, the obligations and the long-term impact of what you are buying. A good property decision is not just about securing finance — it is about securing certainty.

Flash Conveyancing, led by Julian & Renee, understand that in Australia, property ownership is rarely handed over debt-free. It is built over years through mortgages, repayments, equity and careful decision-making. While countries like Romania achieved high outright ownership through historic privatisation, NSW buyers face a very different path — one shaped by lending rules, interest rates, contracts and long-term financial pressure. That is why every property transaction matters. Whether purchasing in Blacktown, Kellyville, Parramatta, Riverstone, The Hills or the Hawkesbury, the goal is not simply to “get into the market”, but to secure an asset that can stand the test of time. From reviewing contracts and title issues to identifying risks before exchange, Julian & Renee help buyers build strong legal foundations so today’s mortgage has the best chance of becoming tomorrow’s genuine ownership.