Lenders Mortgage Insurance (LMI) is one of the most frustrating costs in the property journey for many Australian buyers. It can add thousands of dollars to a loan, often at the very time the buyer is already stretching to cover the deposit, stamp duty, inspections, moving costs and settlement adjustments.

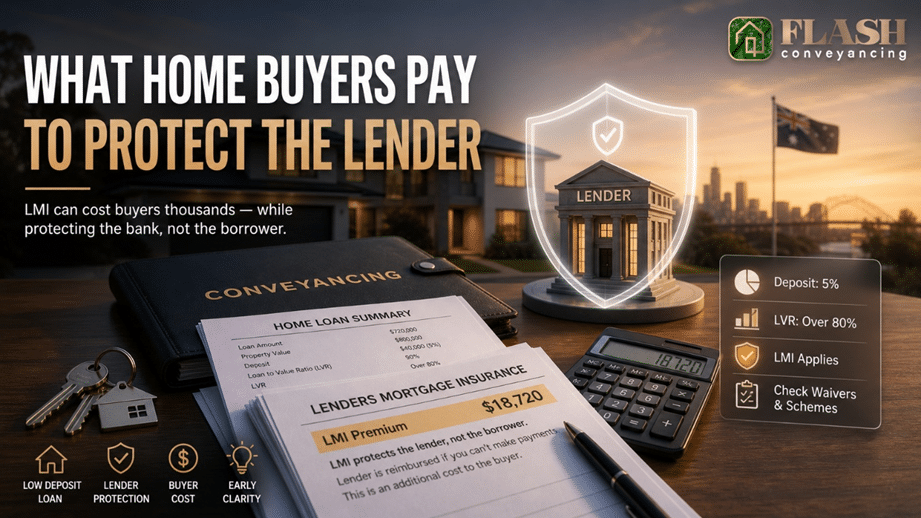

The part that surprises people is simple: LMI isn’t insurance for the buyer. Mortgage insurance is a specialist product that protects the lender if the borrower cannot repay the loan. The premium is usually passed on to the borrower, as the Reserve Bank of Australia explains.

Simply put, LMI is usually required when a buyer has a smaller deposit, generally when the loan-to-value ratio is over 80%. It can help a buyer enter the market sooner, as the bank is more comfortable lending with a lower deposit. But the protection is for the lender, not the person paying the premium.

The frustration comes from that one-sided design. If the borrower defaults and the property is sold for less than the remaining loan balance, the insurer may cover the shortfall for the lender. However, that does not necessarily clear the borrower’s debt. QBE states it can recover the shortfall from the borrower, and ANZ also notes that the LMI provider may pursue the borrower for any loss.

So, the buyer may pay the LMI premium and still remain exposed if the sale proceeds don’t cover the loan. That’s why LMI should never be confused with mortgage protection insurance, income protection or trauma cover. LMI helps the bank manage its lending risk—it does not protect your household if something goes wrong.

Why does the buyer pay for it? A low-deposit loan is considered higher risk by the lender. Even if the bank absorbed the cost, it would likely recover it through higher rates, fees or tighter lending conditions. Charging LMI separately makes the cost visible, but also highlights that the borrower is paying for protection they don’t directly receive.

The good news is that there are more ways for buyers to avoid or reduce LMI in 2026 than many people realise. The Australian Government’s 5% Deposit Scheme (formerly the Home Guarantee Scheme) allows eligible first home buyers to purchase with a 5% deposit without paying LMI. The scheme was expanded from 1 October 2025, with broader access and updated property price caps.

Housing Australia also confirms that eligible single parents or legal guardians may be able to purchase with as little as a 2% deposit without LMI under certain schemes.

Some professionals may also qualify for LMI waivers with particular lenders. For example, NAB notes that eligible professionals in fields such as finance, law and medicine may qualify, subject to criteria, loan type and LVR limits.

The buyer’s practical checklist is straightforward:

- Check with your broker or lender whether LMI applies before signing.

- Check if you are eligible for the 5% Deposit Scheme.

- Ask about professional LMI waivers if your occupation may qualify.

- Confirm whether the LMI premium is paid upfront or capitalised into the loan.

- Be aware that LMI does not protect you from a shortfall claim.

Julian and Renee see how these costs affect real buyers at Flash Conveyancing. A client may have loan approval but still be surprised by the total funds required before settlement. That’s why both the legal and financial aspects of a purchase should be clarified early. Contract terms, deposit timing, finance approval, settlement figures and lender requirements all matter.

Flash Conveyancing is not a replacement for your broker, banker or financial adviser. However, we help you understand the property contract, the settlement process and the legal risks involved. If you are paying LMI, the last thing you need is a rushed contract review or unclear settlement advice.

LMI can be a useful tool if it allows a buyer to enter the market sooner. But it should never be treated as a minor add-on. It is a significant cost attached to a significant loan. Make sure you understand who it protects, what it costs and whether a better structure is available before proceeding.

Flash Conveyancing advice:

Before committing to a low-deposit purchase, ask a sharper question: “Am I paying for speed at the cost of long-term flexibility?” Explore every option—government schemes, lender policies and timing—before you sign, not after. The smartest purchase isn’t just the one you can afford today, but the one that still works for you tomorrow.

Julian & Renee of Flash Conveyancing are specialists in property transactions across NSW. With extensive experience working with local councils including Blacktown, Hawkesbury, Blue Mountains, The Hills, Hornsby and Parramatta, they bring a personal, detail-focused approach to every settlement across Acacia Gardens, Angus, Arndell Park, Blacktown, Colebee, Glendenning, Glenwood, Grantham Farm, Kellyville Ridge, Kings Langley, Marsden Park, Melonba, Oakhurst, Parklea, Quakers Hill, Riverstone, Schofields, Seven Hills, Stanhope Gardens, Tallawong, The Ponds, Baulkham Hills, Beaumont Hills, Bella Vista, Castle Hill, Kellyville, Kenthurst, North Rocks, Northmead, Rouse Hill, Vineyard, Windsor, Annangrove, Box Hill, Cattai, Dural, Gables, Galston, Glenhaven, Glenorie, Maraylya, Middle Dural, Nelson, North Kellyville, Norwest and Winston Hills.