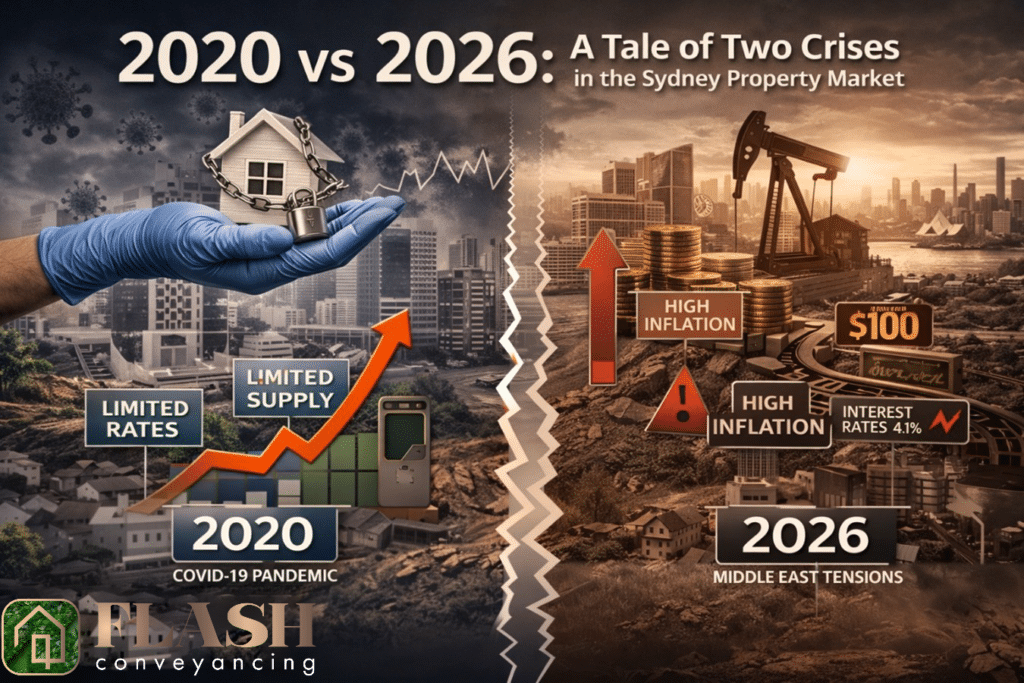

In March 2026, the Sydney property market is once again facing conditions comparable to those seen in 2020. During the COVID-19 pandemic, the market slowed significantly. Now, renewed global uncertainty—particularly linked to tensions in the Middle East—is placing fresh pressure on economic conditions and market sentiment.

The impact of these events is being felt across both homeowners and investors. Unlike 2020, the current environment is characterised by higher inflation, tighter monetary policy, and elevated interest rates, compared to the low-rate, stimulus-driven conditions of the pandemic period. These factors, combined with ongoing energy market volatility, are contributing to rising costs across the economy.

Oil prices have approached $100 per barrel, increasing fuel costs and contributing to higher construction expenses. As a result, the cost of building new homes continues to rise, while the rate of new housing supply is declining. The COVID period demonstrated that supply is a key driver of property prices. In 2021, prices were expected to fall but instead increased, largely due to limited housing stock.

Currently, despite significantly higher interest rates than in 2020, Sydney property prices continue to record annual growth (approximately +6.1%), driven by a substantial national housing shortfall. Property remains a comparatively stable asset class, with investment often shifting towards real estate during periods of market volatility.

The inflationary pressures seen in 2026 differ from those experienced during earlier supply chain disruptions. Construction costs for new homes in Sydney have increased significantly, with fuel and logistics contributing to these rises. Inflation has remained elevated, and the Reserve Bank of Australia is expected to maintain interest rates at or around 4.1% in the near term. This environment requires buyers to carefully assess borrowing capacity before entering into commitments.

Global economic growth is projected at approximately 3.2%, although rising energy costs may increase recession risks. Sydney’s rental market continues to experience low vacancy rates (around 1.1%), supporting rental prices. Even in the event of a technical recession—defined as two consecutive quarters of negative economic growth—property prices are unlikely to experience significant declines due to the ongoing imbalance between supply and demand.

Flash Conveyancing estimates that Sydney house prices may grow by around 5.8% by the end of 2026, representing more moderate growth compared to the COVID period. Buyer behaviour is also expected to shift, with increased preference for established properties with clear title over higher-risk off-the-plan developments. With interest rates remaining elevated, there may be a limited window of reduced competition, providing opportunities for prepared buyers.

Flash Conveyancing Advice

Be prepared to hold property investments over the long term. Ensure contracts include protections. Prioritise properties with approved works or renovations in uncertain market conditions

Julian and Renee of Flash Conveyancing are specialists in property transactions across New South Wales. With experience working with councils including Blacktown, Hawkesbury, Blue Mountains, The Hills, Hornsby, and Parramatta, they provide a tailored and detail-oriented approach to each settlement. Whether you are buying or selling in Acacia Gardens, Marsden Park, Glenwood, Kellyville Ridge, Oakhurst, Bella Vista, Rouse Hill, Windsor, or across Greater Sydney, your transaction will be managed with professionalism and care at every stage.